Property tax revenue is the main source of income for the district: It’s what we use to pave roads, replace pipes, build infrastructure, run programs, and pay staff to do all of the above.

People tend to dislike paying taxes, but they usually enjoy the benefits of having paid taxes. Council tries to keep taxes as low as possible, consistent with staying on top of things like infrastructure maintenance and keeping the district running. Previous councils arguably haven’t kept up with demand, which translated into this council’s 8% tax increases in 2015 and 2016 (dropping to 2% for the rest of the five-year budget).

So here’s a tax issue i’ve been wrestling with: permissive tax exemptions. That’s when council decides to exempt certain properties from the property tax that every landowner pays to the district each year, because those properties are perceived to offer a benefit to the community at large.

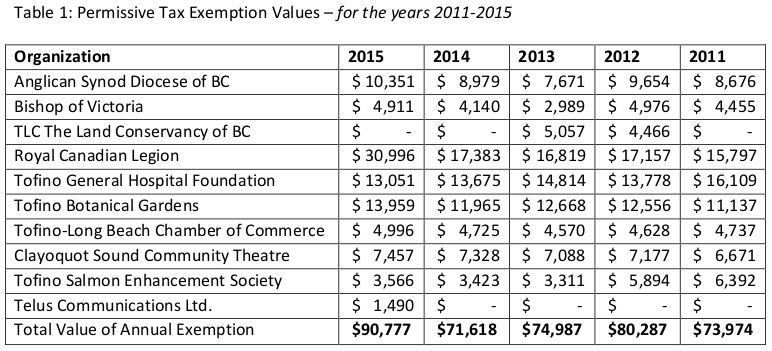

Here’s a table of the Tofino properties historically granted tax exemptions, and their associated amounts for the past several years. (cribbed from the 7-page report (viewable here) that was included in thee 26-April council agenda).

These are the churches and other public service groups that own land. (TLC is for the Monk’s Point property, and the Telus one covers a district right-of-way on the downtown Telus lot.)

Here are a few things i’m wondering about:

-

How much is too much? As you can see from the chart, the amount of tax exemption awarded has been generally trending upward. It jumps around because of changes in the use or assessed value of the individual properties. Some of us on council are concerned that it’s getting kind of high. The district’s total property tax revenue (2016) will be about $3.675 million, so the $90,777 exemption is about 2.5% of the tax revenue. This is not “lost” revenue, it is simply spread amongst all the other taxpayers in town, residential and commercial.

Some other towns investigated by staff in the report linked above don’t put a cap on their tax exemptions. Victoria is an exception, and they limit it to 1.6% of the total tax requisition. If Tofino were to do this, the total exemption would be about $58,800, meaning the organizations listed above would have to collectively cough up about $32,000 in property tax among them. I’m hearing this is a scary prospect for these non-profits, which begs the question, Why upset the apple cart? Which leads to my next question:

-

Is it fair? To quote from the City of Victoria policy (link): “8. A tax exemption is similar in effect to a cash grant….” To me this begs a question of fairness. We have many non-profits in town. Some own real estate, and hold their activities there; some don’t, and rent or borrow a facility to hold their events. Seen in one light, a tax exemption is a district grant, and a pretty substantial one, to a land-owning group. We’ve got, for instance, at least three church groups in town. Two of them get tax exemption “grants,” one doesn’t. So is it fair to give this benefit to certain groups, but not to others.

-

Who benefits? These tax exemptions are granted on the basis of “community benefit.” Some of these venues are open to the public, some serve a small, specific group of residents, and some sit in the middle ground. What scope of “community benefit” should apply, before a group deserves a tax exemption?

To pick on churches again, theoretically anyone can join a church, but that’s a major life decision that doesn’t happen often. So each of our churches directly serve a relatively small silo of the community. On the other hand, some do good works that benefit wider society, so they deserve a break. But many non-landowning groups do the same; should they have access to equivalent grants?

-

Who deserves a tax exemption? Council makes the formal decision, but really it’s up to all Tofino taxpayers, since they are the ones ponying up an extra 2.5% on their tax bills to cover the tax exempt properties. Is the community benefit worth it to you?

I’m still waffling on this one. Our Taxation Exemption Bylaw doesn’t have a stated “policy rationale” to help figure this out. The Victoria bylaw does include a policy rationale: The intent of this policy … is to identify the services and organizations which are the most complementary extensions of municipal services, and for which the burden resulting from the exemption is a justifiable expense to the taxpayers of Victoria. Support should be directed towards services the City would consider providing given adequate resources.

That’s a starting point, but IMHO it leans pretty heavily toward social and other services, and doesn’t capture the community-building aspects of some of the above organizations.

So that’s what i’ve been wondering about this month.